Introduction

Loan lene me aksar banks ya lenders guarantor mangte hain. Guarantor ka role simple hai — agar borrower loan nahi chukata, toh guarantor repayment ki liability le sakta hai. Lekin India me iska legal framework kya hai? Aur agar aap kisi ke loan ke guarantor bane ho, toh default situation me kya legal action ho sakta hai aur aapke rights kya hain?

Is blog me hum Hinglish me step-by-step guide, real-life example, aur FAQs ke saath sab samjhayenge.

( Home Loan Sanction Delay Ho Raha Hai? Kaise Fast Kare, Full Details ➡️ )

Real-Life Example

Ram ne 5 lakh ka personal loan liya, aur Rohan uska guarantor bana. 6 mahine ke liye Ram regular EMI chukata raha, lekin 7th month se payment delay hone laga. Bank ne sabse pehle Ram ko notice bheja, fir Rohan ko inform kiya.

Ye situation har borrower/guarantor ke liye relatable hai, aur isse hum legal responsibilities ko samjh sakte hain.

Guarantor Ka Role Kya Hai?

Guarantor wo banda hai jo borrower ki repayment guarantee karta hai. Agar borrower default karta hai, lender legally guarantor se paisa maang sakta hai.

Official Reference: RBI Guidelines on Guarantors

Loan Default Ka Matlab Kya Hai?

Loan default tab hota hai jab borrower apni EMI time par nahi chukata. 90+ days ke delay par account ko default mark kiya jata hai.

Consequences:

- Credit score damage

- Recovery notices

- Legal action (SARFAESI / civil court)

Guarantor Ki Legal Liability

1) Notice Bheja Ja Sakta Hai

Bank pehle borrower ko notice bhejta hai, fir guarantor ko inform karta hai. Notice me hota hai:

- Outstanding amount

- Days delayed

- Repayment demand

2) Payment Demand

Lender guarantor se repayment legally maang sakta hai, chahe court order na ho.

Legal Action Kaise Ho Sakta Hai?

SARFAESI Act

Bank SARFAESI Act ke tahat:

- Property attach kar sakta hai

- Assets sell kar sakta hai

Reference: SARFAESI Act Full Text

Civil Court

Agar guarantor payment nahi karta, bank civil court me suit file kar sakta hai for recovery.

Guarantor Ke Rights

✔ Right to Notice

Lender pehle borrower ko notice dega aur fir guarantor ko inform karega.

✔ Right to Subrogation

Agar guarantor ne payment kiya, fir wo borrower se recovery claim kar sakta hai.

✔ Right to Information

Loan terms aur proceedings ke bare me clear information milna mandatory hai.

Common Mistakes Jo Guarantor Ko Avoid Karne Chahiye

- Bina document samjhe sign karna

- Loan purpose ignore karna

- Notices ignore karna

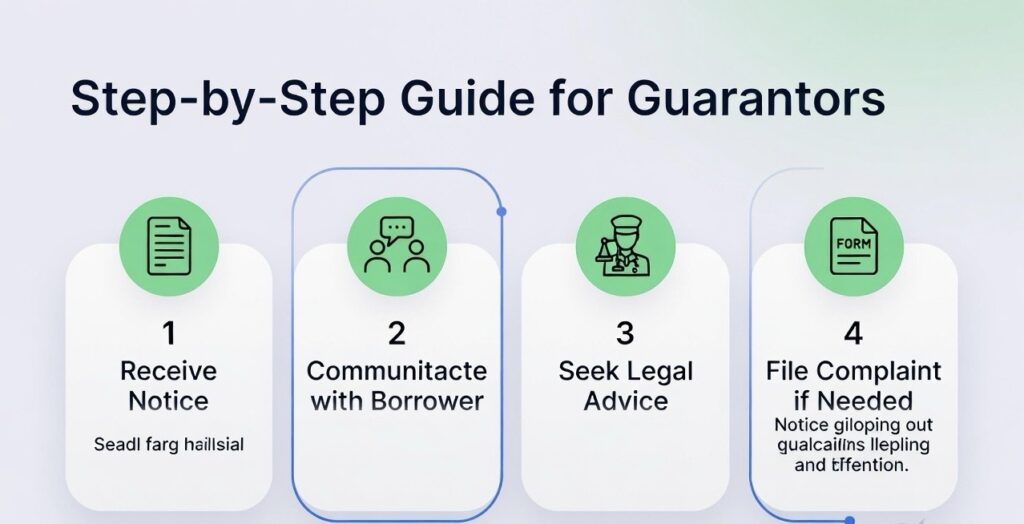

Step-by-Step Guide for Guarantors

- Notice receive hote hi respond karein – Bank aksar plan ya extension provide karta hai

- Borrower se communication maintain karein – Repayment plan discuss karein

- Seek legal advice – Qualified lawyer se consult karein

- File complaint if needed – Banking Ombudsman me complaint file kar sakte hain: Banking Ombudsman

FAQs

Q1: Guarantor notice ignore kar sakta hai kya?

A: Nahi, notice ignore karne se legal risk badhta hai. Response dena zaruri hai.

Q2: Agar borrower ne paisa chukaya, guarantor ka liability khatam ho jata hai kya?

A: Haan, agar borrower repayment karta hai, guarantor ki responsibility automatically khatam ho jati hai.

Q3: SARFAESI Act guarantor pe kaise apply hota hai?

A: Agar borrower default karta hai, lender guarantor se bhi repayment demand kar sakta hai. Legal notices aur property attachment Act ke tahat possible hai.

Conclusion

( Personal Loan Lene Se Pehle Ye 7 Galtiyan Kabhi Na Kare, Full details ➡️ )

Loan me guarantor banna serious responsibility hai. Default hone par SARFAESI Act ya civil court ke tahat lender action le sakta hai, lekin guarantor ke bhi rights hote hain. Terms ko dhyan se samjho, documents carefully padho, aur zarurat pade toh legal expert se consult karo.

Actionable Tip: Apne rights aur responsibilities ke liye expert guidance lein aur notices ko ignore na karein.