Agar aapne loan liya hai aur repayment me problem aa rahi hai, toh bank aksar do options deta hai — Loan Settlement ya Loan Closure. Bahut log in dono ko same samajh lete hain, lekin reality me inka legal aur financial impact bilkul alag hota hai.

Is guide me hum simple Hinglish me samjhenge ki settlement aur closure me kya difference hai, CIBIL score par kya effect padta hai, aur kaunsa option future ke liye safe hota hai.

Loan Closure Kya Hota Hai?

Loan closure ka matlab hota hai ki aapne apna loan completely repay kar diya hai — including principal amount, interest aur charges.

Is situation me:

- Bank aapko No Due Certificate deta hai

- Loan account “Closed” status me update hota hai

- Aapka credit history positive rehta hai

Ye sabse safe aur financially healthy option maana jata hai.

Loan Settlement Kya Hota Hai?

Loan settlement tab hota hai jab borrower poora loan repay nahi kar pata aur bank negotiation ke through partial payment accept karta hai.

Example:

Agar loan baki hai ₹1,00,000 aur bank ₹60,000 lekar account close kar deta hai, toh ise settlement kaha jata hai.

Bank loss accept karta hai, isliye account “Settled” status me report hota hai.

Settlement vs Loan Closure – Main Difference

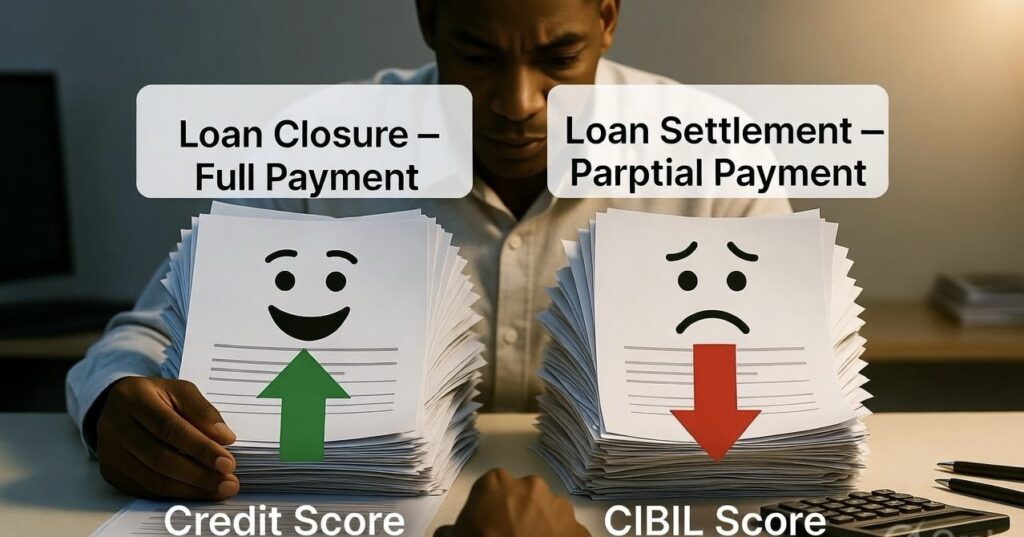

Loan Closure:

- Full payment hoti hai

- Credit score improve hota hai

- Future loan approval easy

Loan Settlement:

- Partial payment hoti hai

- CIBIL score negatively impact hota hai

- Future me loan reject ho sakta hai

CIBIL Score Par Kya Impact Padta Hai?

Loan closure me aapka repayment record strong dikhta hai, jo credit score ko improve karta hai.

Lekin settlement status credit report me years tak visible rehta hai aur banks ise risky borrower signal mante hain.

Aap apna credit report official website par check kar sakte ho:

https://www.cibil.com

Kab Settlement Karna Sahi Hai?

Settlement tab consider kare jab:

- Income loss ya financial emergency ho

- EMI pay karna impossible ho

- Legal recovery risk ho

Lekin agar possible ho, toh pehle restructuring ya EMI modification request karna better hota hai.

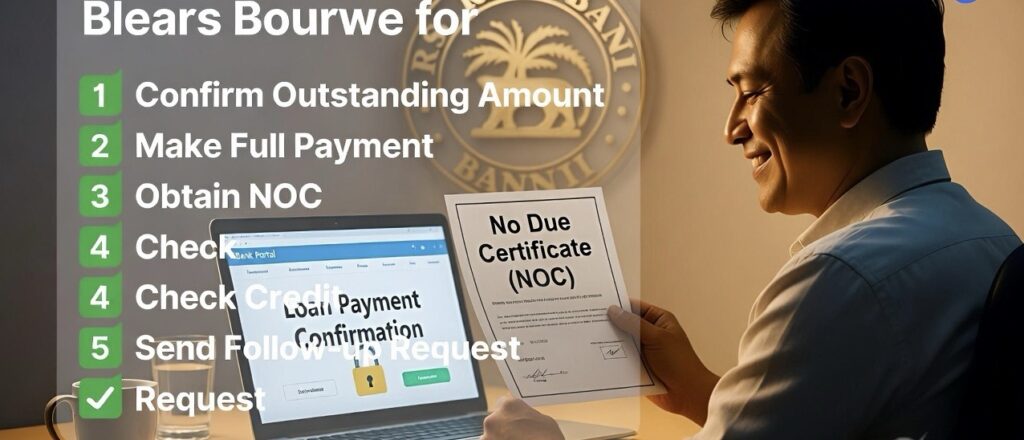

Loan Properly Close Kaise Kare? (Step-by-Step)

- Bank se final outstanding amount confirm kare

- Full payment kare

- No Due Certificate (NOC) le

- Credit report 30–45 din baad check kare

- Agar update na ho toh bank ko written request bheje

RBI Rules Kya Kehte Hain?

RBI guidelines ke according banks ko fair recovery practices follow karni hoti hain aur borrower ko repayment options explain karne hote hain.

Official RBI information:

https://www.rbi.org.in

Final Advice

Short-term relief ke liye settlement easy lag sakta hai, lekin long-term financial future ke liye loan closure hamesha better option hota hai. Decision lene se pehle credit score aur future borrowing plans zaroor consider kare.