Agar aapko bank ya loan company ki taraf se legal notice mila hai, toh sabse pehle panic mat karein. India me legal notice ka matlab jail ya turant case nahi hota. Ye ek official warning hoti hai jisme bank payment ya response demand karta hai.

Is guide me hum simple language me samjhenge ki legal notice aane ke baad kya karna chahiye aur aapke rights kya hain. Banking rules aur borrower protection guidelines Reserve Bank of India (RBI) ke framework par based hote hain.

Bank Legal Notice Kyu Aata Hai?

Bank legal notice usually tab bhejta hai jab EMI 2–3 mahine tak unpaid ho, loan default ho gaya ho, credit card dues pending ho ya bank contact kar raha ho lekin borrower response nahi de raha ho. Legal notice ka main purpose borrower ko legal action se pehle final chance dena hota hai.

- EMI 2–3 mahine tak unpaid ho

- Loan default ho gaya ho

- Credit card dues pending ho

- Bank contact kar raha ho lekin response na mile

Legal Notice Milte Hi Sabse Pehle Kya Kare?

Legal notice milte hi panic karne ki jagah situation ko samajhna zaroori hai.

Step 1: Notice ko dhyan se padhein — loan amount, due amount aur deadline check karein.

Step 2: Notice ignore bilkul na karein — ignore karna situation ko serious bana deta hai.

Step 3: Documents collect karein — loan agreement, payment receipts aur bank messages ready rakhein.

Step 4: Written reply dene ki planning karein — borrower legally reply kar sakta hai.

( EMI miss hone par FIR ka sach kya hai — myths aur facts yaha padhein )

Kya Bank Direct Case Kar Sakta Hai?

Normally bank directly court nahi jaata. Ek proper recovery process follow kiya jata hai:

- Reminder calls

- Legal notice

- Settlement discussion

- Arbitration ya civil recovery process

Loan default generally civil matter hota hai. Criminal case tabhi hota hai jab fraud ya intentional cheating prove ho.

Legal Notice Ka Reply Kaise Kare?

Legal notice ka reply dena borrower ka important right hai. RBI guidelines ke according borrower ko fair communication ka right hota hai. Official complaint system yahan available hai:

RBI Complaint Management System (CMS)

- Apni financial problem explain karein

- Payment plan ya settlement request karein

- Extra charges ka clarification maangein

- Written communication prefer karein

Email ya registered post se reply bhejna safest mana jata hai.

Borrower Ke Legal Rights India Me

India me borrower ke kuch important legal rights hote hain:

- Harassment allowed nahi hai

- Recovery agent abuse nahi kar sakta

- Late night calls illegal hain

- Written statement maangne ka right hota hai

Agar pressure ya threat diya jaye toh borrower complaint file kar sakta hai.

( Loan recovery harassment se kaise bache — RBI rules yaha samjhein )

Complaint Kahan Kare?

Agar bank ya recovery agent unfair behave kare toh yahan complaint ki ja sakti hai:

- Bank grievance department

- RBI Complaint Portal

- National Consumer Helpline

- Consumer Court

Official complaint online bhi easily file ki ja sakti hai.

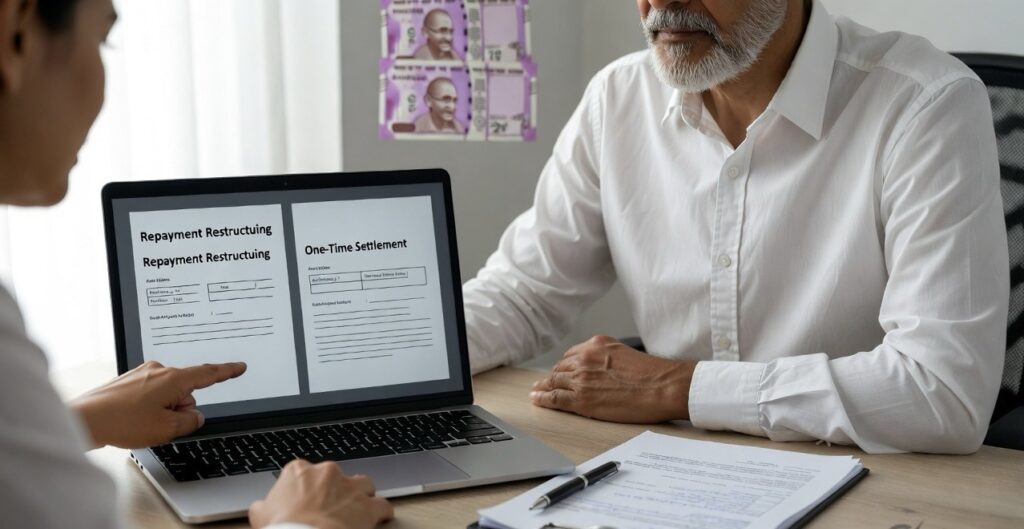

Settlement Karna Better Hai Ya Fight?

Situation ke according decision lena chahiye:

→ Income issue temporary ho toh restructuring request karein

→ Repayment possible na ho toh One Time Settlement discuss karein

Har situation me written agreement lena bahut zaroori hota hai.

Common Mistakes Jo Log Karte Hain

- Notice ignore karna

- Unknown agents ko payment dena

- Cash payment karna

- Legal advice liye bina documents sign kar dena

Final Advice

Legal notice end nahi hota, balki problem solve karne ka ek opportunity hota hai. Calm rahein, timely reply karein aur negotiation try karein. Proper communication se majority cases court tak nahi pahuchte.